ULCER INDEX AND SERENITY RATIO: CAN THEY HELP TO SELECT BETTER PERFORMERS?

Oct 2021, By Vincenzo Taddeo

Introduction:

In this article we will evaluate the usefulness of the Ulcer Index and Serenity Ratio when selecting funds. We will first explain the two metrics and how are they related and then evaluate to what extent Serenity Ratio can outshine the Sharpe Ratio when selecting best performers.

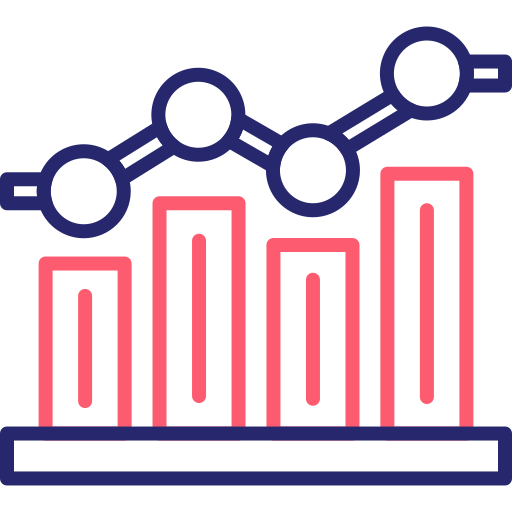

The Serenity Ratio is an alternative measure to the Sharpe Ratio that accounts for extreme risk. While the latter only divides return premium by the annualized volatility, the Serenity Ratio uses the Ulcer Index and a Pitfall Indicator (PI) as risk measures to quantify the tendency of a fund to be “stuck” in drawdown.

To read more, please fill out the form below...

640+

Users

10+

Awards

170+

Companies

$1.5tn+

AuM Worldwide